The IRS said this week that employers will be able to exclude certain items from their gross receipts solely for determining eligibility for the Employee Retention Credit (ERC).

Revenue Procedure 2021-33 provides a safe harbor permitting employers to exclude certain amounts from gross receipts solely for determining eligibility for the ERC. These amounts are:

- The amount of the forgiveness of a Paycheck Protection Program (PPP) Loan;

- Shuttered Venue Operators Grants under the Economic Aid to Hard-Hit Small Businesses, Non-Profits, and Venues Act; and

- Restaurant Revitalization Grants under the American Rescue Plan Act of 2021.

An employer can apply the safe harbor by excluding these amounts only for determining whether it is an eligible employer for a calendar quarter for the purpose of claiming the ERC on its employment tax return.

Revenue Procedure 2021-33 requires employers to apply the safe harbor consistently for determining eligibility for the ERC. The employer must exclude the amounts from their gross receipts for each calendar quarter in which gross receipts are relevant to determining eligibility to claim the ERC. The employer claiming the credit must also apply the safe harbor to all employers treated as a single employer under the aggregation rules.

An employer is not required to apply this safe harbor, and the safe harbor does not permit the exclusion of these amounts from gross receipts for any other federal tax purpose.

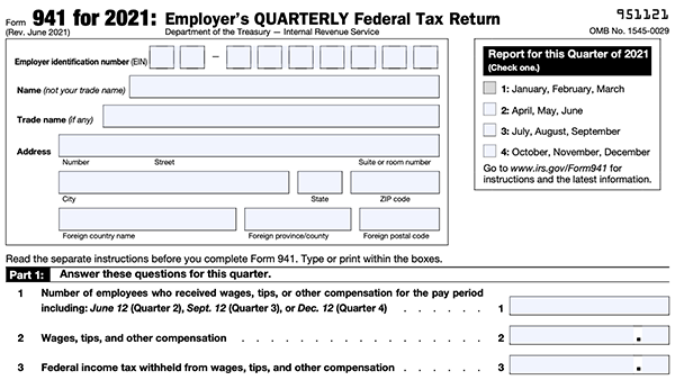

Employers claim the ERC on their employment tax return, generally Form 941, Employers Quarterly Federal Tax Return or adjusted employment tax return, generally Form 941-X, Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund.