Despite a relatively successful 2019, New Jersey businesses are showing a decidedly more concerned outlook and conservative approach for 2020, according to NJBIA's 61st Annual Business Outlook Survey released today.

Despite a relatively successful 2019, New Jersey businesses are showing a decidedly more concerned outlook and conservative approach for 2020, according to NJBIA's 61st Annual Business Outlook Survey released today.

Reflecting on 2019, member businesses reported gains in sales, profits and purchases for the year – although at lower rates than in 2018.

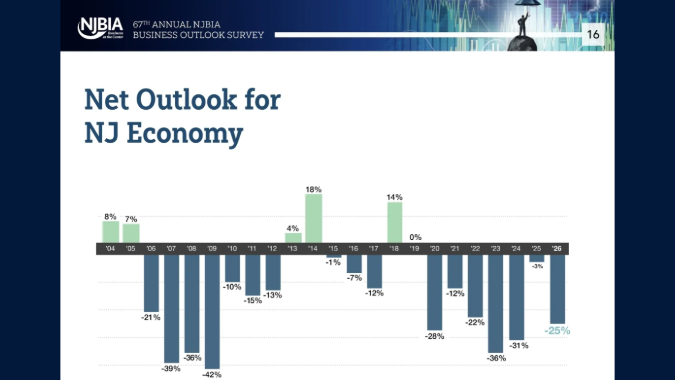

Looking ahead, more than half of respondents forecasted a recession in 2020 or 2021. Meanwhile, the outlook for New Jersey's economy for the first six months of the new year is the lowest it has been in a decade – when the state and the nation were in the midst of the Great Recession.

"While New Jersey businesses continue to have solid returns, there is no question they are feeling the weight of increased costs and mandates," said NJBIA President and CEO Michele Siekerka.

"We can ascertain from these responses that New Jersey's challenging business climate, coupled with the many forecasts of an economic slowdown, are giving our business owners pause for what's ahead."

Among the key findings in NJBIA's 2020 Business Outlook Survey:

- Only 12% reported the New Jersey economy will fare better in the first six months of 2020 than in 2019, while 40% said it will be worse. The -28% net outlook for the state's economy is the lowest since 2009.

- For the U.S. economy, 32% forecasted a better first six months of 2020, compared to 25% who reported it will be worse. The +7% net difference marks a steep decline from the very positive outlooks for 2019 (49%) and 2018 (46%).

- A combined 56% of respondents forecasted a recession in 2020 or 2021.

- Those forecasting an economic slowdown have plans to address it: 62% said they will reduce operational costs, 50% plan to grow their customer base, 35% will postpone hiring and 32% will stall raises.

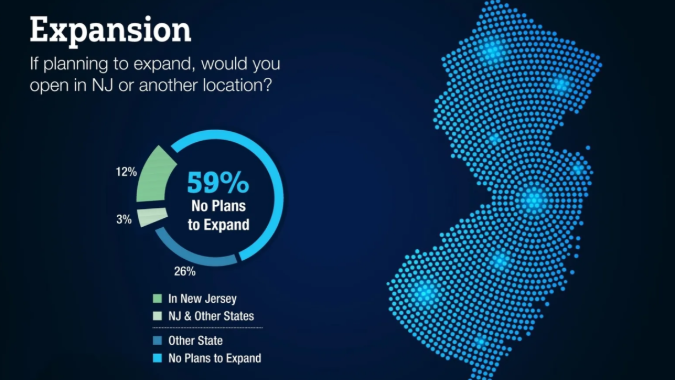

- Only 14% said they would open another location in New Jersey, while 30% said they would choose to expand in another state, with the balance having no plans for expansion at all.

- As a location for new or expanded facilities, New Jersey was listed as very good or good by 21% of respondents, while 41% described it as fair and 38% ranked it as poor.

"New Jersey's affordability and regional competitiveness continue to be challenged," Siekerka added. "While our greatest assets like our schools and workforce continue to rank high, the factors driving our ability to afford those assets continue to be even more expensive and of greater concern year over year.

"This is why NJBIA continues to call for a reform agenda in order to get these outlier costs under control, especially right now with concerns of a recession on the horizon."

New Jersey's Competitiveness

On the positive side, New Jersey's greatest assets continue to shine. Education continued to receive high marks with 49% rating the quality of public schools in New Jersey better than other states – a 5% jump from last year.

Quality of workforce (with 29% saying its better) and ranking New Jersey as a better place to live (24%) are both up slightly from last year. Another 22% say New Jersey is better than other states at protecting the environment – the same number as last year.

But New Jersey's rankings continue to tumble when it comes to the costs, making New Jersey even more of an outlier than just last year.

For example, 89% reported the Garden State worse than other states for taxes and fees. Other cost areas of high concern are controlling government spending (79%), attracting new business (68%), controlling healthcare costs (67%), controlling labor costs (65%), the cost of regulatory compliance (62%), and attitude toward business (60%).

In each of these areas, the rankings were lower than last year's - and in some cases, by a considerable margin.

Employment

A combined 27% said employment in their company increased in 2019, compared to 10% who reported a decrease in employment. That's a net positive of +17%, which is slightly down following last year's +19% net positive in employment.

While the hiring outlook for individual companies appears positive, it lags considerably from 2019. A total of 30% expect to increase employment either substantially or moderately in 2020, compared to 9% who anticipate a moderate or substantial decrease in employment. However, the +21% net positive is lower than the +32% net positive outlook in employment from a year ago.

Sales

Year-over-year actual sales for member businesses remained consistent. In 2019, 54% said sales had increased by varying percentages, compared to 18% that reported fewer sales. That +36% differential is the same net positive disclosed by member businesses in 2018.

Looking ahead, the overall prediction is that sales will slow. While a total of 54% anticipate increased sales in 2020, 14% foresee lower sales. The +40% net positive outlook is a marked decline from the outlooks of 2019 (+53%) and 2018 (+49%).

Profits

Net earnings were strong for member companies with 48% reporting profits for the year, compared to 23% recording a loss. The net positive of +25% this year is consistent with the +26% showing by businesses in 2018, and a sizable increase from 2017 (+18%) and 2016 (+3%).

A total of 49% predict profits in 2020, while 17% envision a loss. The net positive of 32% is a sizable drop from the forecasts for 2019 (46%) and 2018 (43%).

Purchases and Prices

Price increases by businesses, perhaps compensating for costs of new workplace mandates, continue to be a trend. One percent of respondents said they substantially increased prices of their primary products and services, while another 48% said they had moderate increases. Only 3% said they decreased prices moderately or substantially.

That +46% change is a sharp increase from 2018 (+38%) and 2017 (+29%).

Members maintain optimism about their future purchasing plans, with 43% expecting to increase the dollar value of their purchases in 2020 and 15% anticipating a decline. This net positive of +28% is down slightly from 2019 projections (+32%) and even more so than 2018 forecasts (+39%).

Wages

In 2019, 77% of member companies gave pay increases – a typical number for this survey. The average increase was 2.9%. A combined total of 16% gave an average raise of 5% or more, while 33% of respondents doled out increases between 3% and 4.9%.

For planned pay raises in 2020, 34% plan to provide a bump between 1% and 2.9%. Only 12% plan on giving raises of 5% or more in 2020 – compared to the 16% who gave raises in the same range in 2019.

Minimum Wage and Cannabis

Looking ahead to Year Two of the five-year phase-in of the $15 minimum wage, 51% expect it to impact their business. Of those respondents, 32% say they will raise prices, 21% will reduce staff, 15% will reduce benefits and 13% will look toward automation.

When asked if they felt the potential legalization of recreational cannabis would be good for the state economy, 44% of respondents said yes and 56% said no.

More than two-third (67%) of business owners said they had concerns about legalized recreational cannabis. Of those respondents, 84% said their considerations revolved around safety in the workplace and 75% said workforce productivity was a concern. Chronic absenteeism (45%) and proximity to dispensaries (17%) were also noted.

About the Survey

Questions for NJBIA's 61st Annual Business Outlook Survey were sent to member business owners in September 2019. The report is based on 878 valid responses. Most respondents were small businesses, with 61% employing fewer than 24 employees.